When Full Coverage Stops Earning Its Cost

You opened your Cape Coral renewal notice and the premium climbed again, though you drive the same paid-off sedan 6,000 miles a year and carry the same clean record you've held for decades. The carrier still charges you for collision and comprehensive on a vehicle whose trade-in value dropped below $4,000 two years ago, and no one has asked whether you still want them.

This is the coverage-fit friction retirees hit harder than any other age bracket. Full coverage made sense when you financed the car and the lender required it. Now the car is yours, your annual mileage is a third of what it was during your working years, and the gap between what you pay and what a totaled vehicle would return keeps widening. Most agents never surface this decision because they assume you know it exists. You don't owe them that assumption.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteFlorida Property Damage Minimum

$10,000

Florida requires $10,000 property damage liability and $10,000 PIP, but does not mandate bodily injury liability for in-state drivers. This is the floor you cannot drop below, regardless of your vehicle's value or age.

Florida auto_insurance_state_data

What Full Coverage Actually Protects

Full coverage is shorthand for a liability-plus-physical-damage bundle: liability (bodily injury and property damage) protects assets you own if you cause an accident, PIP pays your medical bills up to the state minimum regardless of fault, and collision and comprehensive repair or replace your vehicle after a crash, theft, or weather event. The first three protect you from financial ruin. The last two protect the car itself.

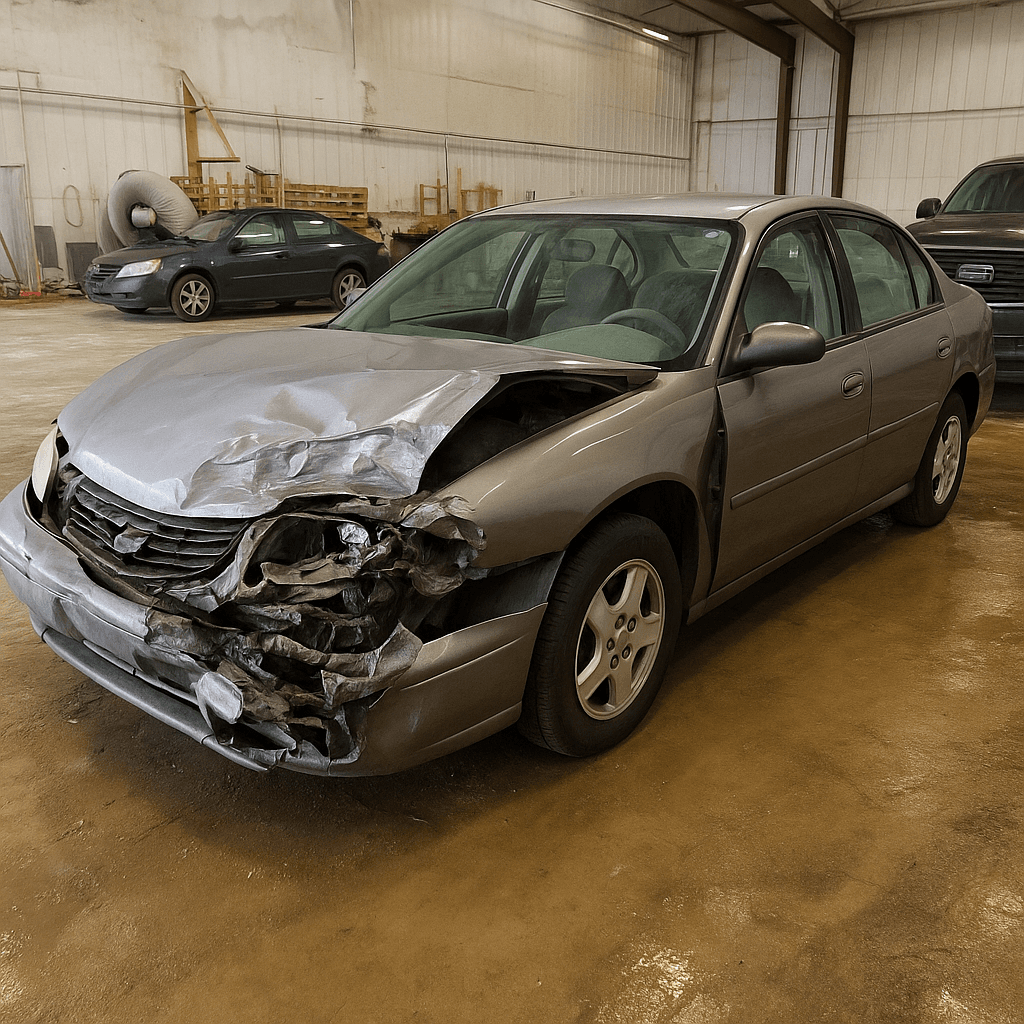

When the car was worth $28,000 and you owed $22,000, collision and comprehensive were non-negotiable. A totaled vehicle would have left you paying off a loan with no car. Now the car is worth $3,800 and you owe nothing. Collision pays the actual cash value minus your deductible. If your deductible is $1,000, a total loss nets you $2,800. If your collision premium runs $400 annually, you're paying that $2,800 ceiling back in seven years—and the value drops every year while the premium holds or rises.

Comprehensive faces the same math. It covers theft, vandalism, fire, flood, and animal strikes. Cape Coral sits in a flood zone, so comprehensive earns more consideration here than in most metro areas. But the payout ceiling is still actual cash value minus deductible. If the car is worth $3,800 and your comprehensive deductible is $500, the maximum check you receive is $3,300. Compare that against your annual comprehensive premium and your flood-risk tolerance. The math is position-specific, not universal.

You're buying replacement protection for an asset whose payout ceiling falls every year while your premium stays flat or climbs. No agent will tell you when to stop.

The Coverage-Fit Decision on a Paid-Off Vehicle

Start with the vehicle's actual cash value today, not what you paid or what you remember from last year's appraisal. Kelley Blue Book and Edmunds provide trade-in values; actual cash value sits slightly above trade-in. Subtract your collision deductible. That remainder is the maximum check you receive if the car is totaled tomorrow. Now divide that remainder by your annual collision premium. The result is the payback period in years. If the payback period exceeds three years, collision is returning less value than it costs in most retiree scenarios.

Repeat the same calculation for comprehensive using your comprehensive deductible and annual comprehensive premium. Comprehensive typically costs less than collision, and Cape Coral's flood exposure tilts the decision slightly toward keeping it longer. But the payback math applies identically. A common outcome for retirees with paid-off vehicles in the $3,000–$5,000 range: drop collision, keep comprehensive one more renewal cycle, then re-evaluate both annually as the value continues falling.

Related Articles

How Florida's Mature-Driver Discount Applies

Florida law requires insurers to offer a mature-driver discount to operators age 55 and older under Fla. Stat. §627.0652. The statute does not fix a percentage; each carrier sets the amount in its filed rate structure. This means the discount exists by mandate, but its size varies across carriers and the only way to verify what yours applies is to ask your agent directly or request a quote breakdown showing the discount line item.

The discount typically triggers automatically at age 55 for most carriers writing in Florida, but some require completion of a state-approved defensive driving course to activate it. The course requirement is carrier-specific, not statutory. Geico, Progressive, State Farm, and Nationwide all write in Florida and offer mature-driver discounts; whether yours requires the course, and how much the discount reduces your premium, depends on the carrier's filed rates. No aggregator shows this transparently. You verify it at quote time.

If you completed a mature-driver course and submitted the certificate to your carrier, confirm the discount appears on your current declaration page. Certificates expire, and most carriers do not re-apply the discount automatically when the certificate lapses. If the discount disappeared at renewal and you did not re-enroll, that is the mechanism. Re-enrollment every three years is standard across Florida carriers requiring the course.

Carriers Writing Cape Coral

25

At least 25 carriers write auto insurance in Florida, including Geico, Progressive, State Farm, Allstate, Nationwide, and non-standard specialists like Dairyland, Acceptance, and The General. Mature-driver discount amounts and low-mileage program availability differ across all of them.

auto_insurance_carriers_by_state

Low-Mileage and Usage-Based Programs

You drive 6,000 miles annually now that the commute is gone. Most retirees in Cape Coral fall into the 5,000–8,000 mile range. Standard pricing assumes 12,000–15,000 miles, so you're subsidizing higher-mileage drivers unless your carrier adjusts for actual use. Two program types address this: low-mileage discounts based on self-reported annual mileage, and usage-based insurance programs that monitor mileage and driving behavior via telematics.

Low-mileage discounts are simpler and require no device. You report your annual mileage at renewal; the carrier applies a tiered discount if you fall below its threshold. Geico, State Farm, and Nationwide all offer mileage-based discounts in Florida. The discount percentage is carrier-specific and not published transparently. Ask your agent what mileage threshold qualifies and what percentage applies. If your current carrier does not offer one, this becomes a comparison point when you shop.

Usage-based programs like Progressive's Snapshot, State Farm's Drive Safe & Save, and Nationwide's SmartRide track mileage, hard braking, and time-of-day driving via a plug-in device or smartphone app. Initial discounts for enrolling range across carriers, and the final discount adjusts after the monitoring period based on actual behavior. Retirees with low annual mileage and minimal night driving typically perform well in these programs, but the telematics requirement is a deal-breaker for some. Evaluate it as a data-sharing decision, not just a discount opportunity.

Medical Payments Coverage and Medicare Coordination

Florida requires $10,000 in personal injury protection, which pays your medical bills after an accident regardless of fault. PIP is primary in Florida, meaning it pays before Medicare. If your accident-related medical costs exceed $10,000, Medicare covers the remainder as secondary payer. This coordination is statutory, not optional, and it means medical payments coverage—an optional add-on that pays medical bills above PIP—duplicates what Medicare already provides for most retirees.

Medical payments coverage made sense before you enrolled in Medicare. Now it sits between PIP and Medicare, covering a gap that Medicare closes automatically. Most retirees in Cape Coral carry it because no one told them to drop it. Review your declaration page. If you see a medical payments line item and you have Medicare Part B, ask your agent whether dropping it changes your premium. The savings are typically modest, but modest cuts compound when you stack them with mileage adjustments and collision removal.

Compare Carriers That Price Retirees Favorably

Carriers differ sharply on how they price low-mileage retirees with clean records and paid-off vehicles. Some apply age as a risk factor that raises rates after 70; others treat mature drivers as a preferred segment and price accordingly. The only way to surface this is to compare quoted premiums with identical coverage inputs across at least four carriers. Request quotes from a standard-market carrier like State Farm or Geico, a preferred-tier carrier like USAA if you qualify or Amica, and a non-standard specialist like Dairyland or Acceptance that writes high-risk but also competes for clean-record seniors seeking budget options.

When you request quotes, provide identical coverage limits, deductibles, and vehicle details to each carrier. Ask each agent to itemize the mature-driver discount, any mileage-based discount, and whether completing a defensive driving course would change the rate further. Write down the discount amounts and the total premium. The carrier offering the lowest total is not always the best fit; the carrier that transparently shows you how it discounts your profile and allows annual re-verification of mileage without penalty often delivers better long-term value.