Updated July 2026

What Is Collision Coverage Insurance?

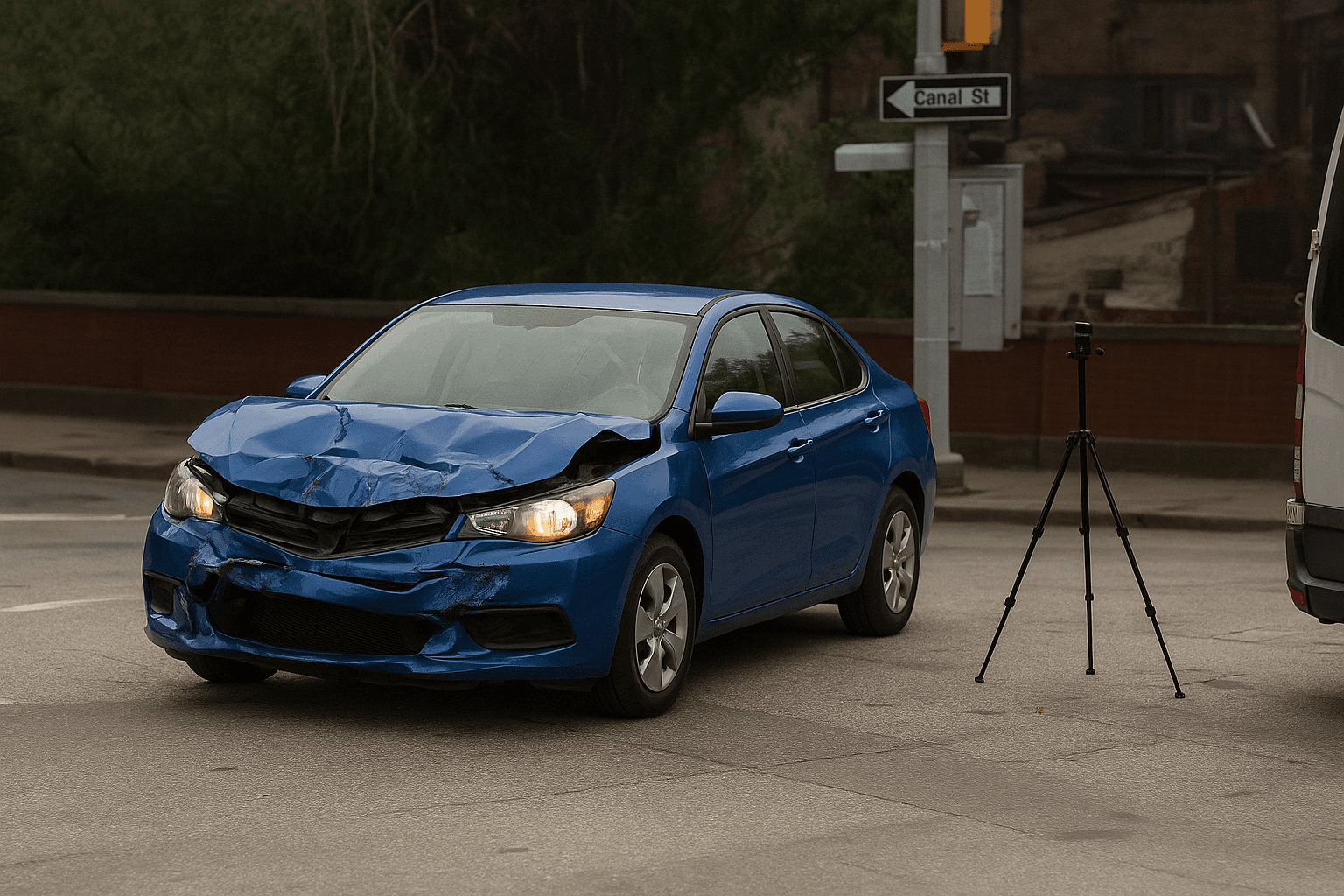

Collision coverage pays to repair or replace your vehicle after a crash with another car, a stationary object like a guardrail or pole, or a rollover — regardless of who caused the accident. Your insurer cuts you a check for repair costs minus your deductible, up to your vehicle's actual cash value at the time of loss. If you caused the crash, collision is the only coverage that pays for your own vehicle damage. If the other driver caused it and carries liability insurance, you can file through their policy instead, but collision lets you start repairs immediately without waiting for fault determination.

- You're at fault. The other driver's vehicle has $6,200 in damage, covered by your liability insurance. Your own car has $4,800 in damage. Collision pays the $4,800 minus your $500 deductible — you receive $4,300. Without collision, you pay the full $4,800 out of pocket. Your liability coverage does not pay for your own vehicle under any circumstance.

- The other driver is at fault and carries liability insurance. You can file a claim through their policy and pay nothing, but their insurer may take weeks to accept fault and issue payment. If you carry collision, you file with your own insurer, pay your $500 deductible, and start repairs within days. Your insurer then recovers the $500 from the at-fault driver's carrier through subrogation and refunds your deductible — typically within 60 to 90 days.

- No other vehicle involved. Repair estimate is $3,400. Collision pays $2,900 after your $500 deductible. If your vehicle is worth $5,000 and repair costs exceed $4,000, most insurers total the car and pay the $5,000 actual cash value minus the deductible. You keep the salvage or let the insurer take possession.

Who Needs Collision Coverage Insurance?

Retirees with financed or leased vehicles must carry collision until the loan is paid. If your vehicle is worth more than $5,000 and you lack the savings to replace it after a crash, collision protects that asset. Drivers who commute in dense traffic or park on streets with higher accident risk benefit from the peace of mind, even on older vehicles.

Compare your vehicle's current actual cash value to three years of collision premiums plus your deductible. If that total exceeds the car's value, dropping collision makes financial sense unless you cannot afford sudden out-of-pocket replacement costs. Drivers in their first year of retirement who just paid off a vehicle should reassess — the coverage that protected a $28,000 asset five years ago may now protect a $6,000 asset at the same annual cost.

How Much Does Collision Coverage Insurance Cost?

Collision adds $30–$60 per month to a Florida retiree's premium, or $360–$720 annually, depending on vehicle value, deductible choice, and driving record.

- Vehicle actual cash value — newer or higher-value vehicles cost more to insure because maximum payout is higher.

- Deductible selection — choosing a $1,000 deductible instead of $500 lowers premium by 15–25 percent.

- Garaging ZIP code — urban counties with higher crash density and repair costs produce higher collision premiums.

- Driving record — at-fault accidents in the past three years increase collision premium by 20–40 percent, even for otherwise clean records.

- Annual mileage — drivers logging under 7,500 miles per year qualify for low-mileage discounts with most carriers, lowering collision cost by 10–20 percent.